Euro

Euro

Jump to navigation

Jump to search

Euro | |||||

|---|---|---|---|---|---|

| евро (Bulgarian), ευρώ (Greek), euró (Hungarian), eoró (Irish), eiro (Latvian), euras (Lithuanian), ewro (Maltese), evro (Slovene) | |||||

| |||||

| ISO 4217 | |||||

| Code | EUR | ||||

| Number | 978 | ||||

| Exponent | 2 | ||||

| Denominations | |||||

| Subunit | |||||

.mw-parser-output .noboldfont-weight:normal 1/100 | cent Actual usage varies depending on language | ||||

| Plural | See Euro linguistic issues | ||||

cent | See article | ||||

| Symbol | € | ||||

cent | c | ||||

| Nickname | The single currency[1], Fiber[2] and others local names

| ||||

| Banknotes | |||||

Freq. used | €5, €10, €20, €50, €100 | ||||

Rarely used | €200, €500 | ||||

| Coins | |||||

Freq. used | 1c, 2c, 5c, 10c, 20c, 50c, €1, €2 | ||||

Rarely used | 1c, 2c (Finland and Netherlands) | ||||

| Demographics | |||||

| Official user(s) |

Monetary agreement (10)

| ||||

| Unofficial user(s) | Other users (2)

Other partial users (1)

Single euro payments area (13 from 35)

| ||||

| Issuance | |||||

| Central bank | European Central Bank | ||||

Website | www.ecb.europa.eu | ||||

| Printer | Several

| ||||

Website | Several

| ||||

| Mint | Several

| ||||

Website | Several

| ||||

| Valuation | |||||

| Inflation | 1.9% (November 2018) | ||||

Source | ecb.europa.eu | ||||

Method | HICP | ||||

| Pegged by | 12 currencies

| ||||

European Union |

|---|

|

This article is part of a series on the politics and government of the European Union |

Member States

Presidency of the Council of the European Union

|

Treaties The Treaties

Treaties of Accession

Other Treaties

Abandoned treaties and agreements

|

Executive European Council

European Commission

|

Legislature European Parliament (Members)

Council of the EU (Presidency)

|

Judiciary European Court of Justice

|

Euro Eurozone Members

Eurogroup

European Central Bank

|

Schengen Area Participating Schengen Area States

|

European Economic Area EEA Members

|

Court of Auditors

|

Other Bodies

Former European Bodies

|

Law

|

Policies and Issues

|

Elections

|

Other Unofficial EU Currencies

Non-Schengen Area States

Candidate Countries for EU Membership

|

Foreign Relations High Representative

Foreign relations of EU Member States

|

|

The euro (sign: €; code: EUR) is the official currency of 19 of the 28 member states of the European Union. This group of states is known as the eurozone or euro area, and counts about 343 million citizens as of 2019[update].[7][8] The euro is the second largest and second most traded currency in the foreign exchange market after the United States dollar.[9] The euro is subdivided into 100 cents.

The currency is also used officially by the institutions of the European Union, by four European microstates that are not EU members,[8] as well as unilaterally by Montenegro and Kosovo. Outside Europe, a number of special territories of EU members also use the euro as their currency. Additionally, 240 million people worldwide as of 2018[update] use currencies pegged to the euro.[citation needed]

The euro is the second largest reserve currency as well as the second most traded currency in the world after the United States dollar.[10][11][12]

As of August 2018[update], with more than €1.2 trillion in circulation, the euro has one of the highest combined values of banknotes and coins in circulation in the world, having surpassed the U.S. dollar.[13][note 14]

The name euro was officially adopted on 16 December 1995 in Madrid.[14] The euro was introduced to world financial markets as an accounting currency on 1 January 1999, replacing the former European Currency Unit (ECU) at a ratio of 1:1 (US$1.1743). Physical euro coins and banknotes entered into circulation on 1 January 2002, making it the day-to-day operating currency of its original members, and by March 2002 it had completely replaced the former currencies.[15] While the euro dropped subsequently to US$0.83 within two years (26 October 2000), it has traded above the U.S. dollar since the end of 2002, peaking at US$1.60 on 18 July 2008.[16] In late 2009, the euro became immersed in the European sovereign-debt crisis, which led to the creation of the European Financial Stability Facility as well as other reforms aimed at stabilising and strengthing the currency.

Contents

1 Administration

2 Issuing modalities for banknotes

3 Characteristics

3.1 Coins and banknotes

3.2 Payments clearing, electronic funds transfer

3.3 Currency sign

4 History

4.1 Introduction

4.2 Eurozone crisis

5 Direct and indirect usage

5.1 Direct usage

5.2 Use as reserve currency

5.3 Currencies pegged to the euro

6 Economics

6.1 Optimal currency area

6.2 Transaction costs and risks

6.3 Price parity

6.4 Macroeconomic stability

6.4.1 Trade

6.4.2 Investment

6.4.3 Inflation

6.4.4 Exchange rate risk

6.4.5 Financial integration

6.4.6 Effect on interest rates

6.4.7 Price convergence

6.4.8 Tourism

7 Exchange rates

7.1 Flexible exchange rates

7.2 Against other major currencies

8 Linguistic issues

9 See also

10 Notes

11 References

12 Further reading

13 External links

Administration[edit]

The European Central Bank has its seat in Frankfurt (Germany) and is in charge of the monetary policy of the eurozone.

The euro is managed and administered by the Frankfurt-based European Central Bank (ECB) and the Eurosystem (composed of the central banks of the eurozone countries). As an independent central bank, the ECB has sole authority to set monetary policy. The Eurosystem participates in the printing, minting and distribution of notes and coins in all member states, and the operation of the eurozone payment systems.

The 1992 Maastricht Treaty obliges most EU member states to adopt the euro upon meeting certain monetary and budgetary convergence criteria, although not all states have done so. The United Kingdom and Denmark negotiated exemptions,[17] while Sweden (which joined the EU in 1995, after the Maastricht Treaty was signed) turned down the euro in a 2003 referendum, and has circumvented the obligation to adopt the euro by not meeting the monetary and budgetary requirements. All nations that have joined the EU since 1993 have pledged to adopt the euro in due course.

Issuing modalities for banknotes[edit]

Since 1 January 2002, the national central banks (NCBs) and the ECB have issued euro banknotes on a joint basis.[18] Euro banknotes do not show which central bank issued them.[dubious ] Eurosystem NCBs are required to accept euro banknotes put into circulation by other Eurosystem members and these banknotes are not repatriated. The ECB issues 8% of the total value of banknotes issued by the Eurosystem.[18] In practice, the ECB's banknotes are put into circulation by the NCBs, thereby incurring matching liabilities vis-à-vis the ECB. These liabilities carry interest at the main refinancing rate of the ECB. The other 92% of euro banknotes are issued by the NCBs in proportion to their respective shares of the ECB capital key,[18] calculated using national share of European Union (EU) population and national share of EU GDP, equally weighted.[19]

Characteristics[edit]

Coins and banknotes[edit]

Euro coins and banknotes of various denominations

Euro banknotes from the Europa series (€100 & €200 notes not yet in circulation)

The euro is divided into 100 cents (sometimes referred to as euro cents, especially when distinguishing them from other currencies, and referred to as such on the common side of all cent coins). In Community legislative acts the plural forms of euro and cent are spelled without the s, notwithstanding normal English usage.[20][21] Otherwise, normal English plurals are sometimes used,[22] with many local variations such as centime in France.

All circulating coins have a common side showing the denomination or value, and a map in the background. Due to the linguistic plurality in the European Union, the Latin alphabet version of euro is used (as opposed to the less common Greek or Cyrillic) and Arabic numerals (other text is used on national sides in national languages, but other text on the common side is avoided). For the denominations except the 1-, 2- and 5-cent coins, the map only showed the 15 member states which were members when the euro was introduced. Beginning in 2007 or 2008 (depending on the country) the old map is being replaced by a map of Europe also showing countries outside the Union like Norway, Ukraine, Belarus, Russia or Turkey. The 1-, 2- and 5-cent coins, however, keep their old design, showing a geographical map of Europe with the 15 member states of 2002 raised somewhat above the rest of the map. All common sides were designed by Luc Luycx. The coins also have a national side showing an image specifically chosen by the country that issued the coin. Euro coins from any member state may be freely used in any nation that has adopted the euro.

The new banknotes were introduced in the beginning of 2013. The top half of the image shows the front side of the 5 euro note and the bottom half shows the back side.

10 euro note from the new Europa series written in Latin (EURO) and Greek (ΕΥΡΩ) alphabets, but also in the Cyrillic (ЕВРО) alphabet, as a result of Bulgaria joining the European Union in 2007.

The design for the new Europa series 100 euro note (and for new 50 and 200 notes) features the acronyms of the name of the European Central Bank in ten linguistic variants, covering all official languages of the EU28.

The coins are issued in denominations of €2, €1, 50c, 20c, 10c, 5c, 2c, and 1c. To avoid the use of the two smallest coins, some cash transactions are rounded to the nearest five cents in the Netherlands and Ireland[23][24] (by voluntary agreement) and in Finland (by law).[25] This practice is discouraged by the Commission, as is the practice of certain shops of refusing to accept high-value euro notes.[26]

Commemorative coins with €2 face value have been issued with changes to the design of the national side of the coin. These include both commonly issued coins, such as the €2 commemorative coin for the fiftieth anniversary of the signing of the Treaty of Rome, and nationally issued coins, such as the coin to commemorate the 2004 Summer Olympics issued by Greece. These coins are legal tender throughout the eurozone. Collector coins with various other denominations have been issued as well, but these are not intended for general circulation, and they are legal tender only in the member state that issued them.[27]

The design for the euro banknotes has common designs on both sides. The design was created by the Austrian designer Robert Kalina.[28] Notes are issued in €500, €200, €100, €50, €20, €10, €5. Each banknote has its own colour and is dedicated to an artistic period of European architecture. The front of the note features windows or gateways while the back has bridges, symbolising links between countries and with the future. While the designs are supposed to be devoid of any identifiable characteristics, the initial designs by Robert Kalina were of specific bridges, including the Rialto and the Pont de Neuilly, and were subsequently rendered more generic; the final designs still bear very close similarities to their specific prototypes; thus they are not truly generic. The monuments looked similar enough to different national monuments to please everyone.[29]

Payments clearing, electronic funds transfer[edit]

Capital within the EU may be transferred in any amount from one country to another. All intra-EU transfers in euro are treated as domestic transactions and bear the corresponding domestic transfer costs.[30] This includes all member states of the EU, even those outside the eurozone providing the transactions are carried out in euro.[31] Credit/debit card charging and ATM withdrawals within the eurozone are also treated as domestic transactions; however paper-based payment orders, like cheques, have not been standardised so these are still domestic-based. The ECB has also set up a clearing system, TARGET, for large euro transactions.[32]

Currency sign[edit]

The euro sign; logotype and handwritten

A special euro currency sign (€) was designed after a public survey had narrowed the original ten proposals down to two. The European Commission then chose the design created by the Belgian Alain Billiet. Of the symbol, the EC stated[20]

.mw-parser-output .templatequoteoverflow:hidden;margin:1em 0;padding:0 40px.mw-parser-output .templatequote .templatequoteciteline-height:1.5em;text-align:left;padding-left:1.6em;margin-top:0

Inspiration for the € symbol itself came from the Greek epsilon (Є)[note 15] – a reference to the cradle of European civilisation – and the first letter of the word Europe, crossed by two parallel lines to 'certify' the stability of the euro.

— European Commission

The European Commission also specified a euro logo with exact proportions and foreground and background colour tones.[33] While the Commission intended the logo to be a prescribed glyph shape[citation needed], font designers made it clear that they intended to design their own variants instead.[34]Typewriters lacking the euro sign can create it by typing a capital "C", backspacing, and overstriking it with the equal ("=") sign. Placement of the currency sign relative to the numeric amount varies from nation to nation, but for texts in English the symbol (or the ISO-standard "EUR") should precede the amount.[35]

History[edit]

Introduction[edit]

This section needs additional citations for verification. (December 2017) (Learn how and when to remove this template message) |

| Country | Currency | Code (ISO 4217) | Rate[36] | Fixed on | Yielded |

|---|---|---|---|---|---|

| Austria | Austrian schilling | ATS | 7001137603000000000♠13.7603 | 1998-12-31 | 1999-01-01 |

| Belgium | Belgian franc | BEF | 7001403399000000000♠40.3399 | 1998-12-31 | 1999-01-01 |

| Cyprus | Cypriot pound | CYP | 6999585274000000000♠0.585274 | 2007-07-10 | 2008-01-01 |

| Netherlands | Dutch guilder | NLG | 7000220371000000000♠2.20371 | 1998-12-31 | 1999-01-01 |

| Estonia | Estonian kroon | EEK | 7001156466000000000♠15.6466 | 2010-07-13 | 2011-01-01 |

| Finland | Finnish markka | FIM | 7000594573000000000♠5.94573 | 1998-12-31 | 1999-01-01 |

| France | French franc | FRF | 7000655957000000000♠6.55957 | 1998-12-31 | 1999-01-01 |

| Germany | German mark | DEM | 7000195583000000000♠1.95583 | 1998-12-31 | 1999-01-01 |

| Greece | Greek drachma | GRD | 7002340750000000000♠340.75 | 2000-06-19 | 2001-01-01 |

| Ireland | Irish pound | IEP | 6999787564000000000♠0.787564 | 1998-12-31 | 1999-01-01 |

| Italy | Italian lira | ITL | 7003193627000000000♠1,936.27 | 1998-12-31 | 1999-01-01 |

| Latvia | Latvian lats | LVL | 6999702804000000000♠0.702804 | 2013-07-09 | 2014-01-01 |

| Lithuania | Lithuanian litas | LTL | 7000345280000000000♠3.4528 | 2014-07-23 | 2015-01-01 |

| Luxembourg | Luxembourgish franc | LUF | 7001403399000000000♠40.3399 | 1998-12-31 | 1999-01-01 |

| Malta | Maltese lira | MTL | 6999429300000000000♠0.4293 | 2007-07-10 | 2008-01-01 |

| Monaco | Monégasque franc | MCF | 7000655957000000000♠6.55957 | 1998-12-31 | 1999-01-01 |

| Portugal | Portuguese escudo | PTE | 7002200482000000000♠200.482 | 1998-12-31 | 1999-01-01 |

| San Marino | Sammarinese lira | SML | 7003193627000000000♠1,936.27 | 1998-12-31 | 1999-01-01 |

| Slovakia | Slovak koruna | SKK | 7001301260000000000♠30.126 | 2008-07-08 | 2009-01-01 |

| Slovenia | Slovenian tolar | SIT | 7002239640000000000♠239.64 | 2006-07-11 | 2007-01-01 |

| Spain | Spanish peseta | ESP | 7002166386000000000♠166.386 | 1998-12-31 | 1999-01-01 |

| Vatican City | Vatican lira | VAL | 7003193627000000000♠1,936.27 | 1998-12-31 | 1999-01-01 |

The euro was established by the provisions in the 1992 Maastricht Treaty. To participate in the currency, member states are meant to meet strict criteria, such as a budget deficit of less than 3% of their GDP, a debt ratio of less than 60% of GDP (both of which were ultimately widely flouted after introduction), low inflation, and interest rates close to the EU average. In the Maastricht Treaty, the United Kingdom and Denmark were granted exemptions per their request from moving to the stage of monetary union which resulted in the introduction of the euro. (For macroeconomic theory, see below.)

The name "euro" was officially adopted in Madrid on 16 December 1995.[14] Belgian Esperantist Germain Pirlot, a former teacher of French and history is credited with naming the new currency by sending a letter to then President of the European Commission, Jacques Santer, suggesting the name "euro" on 4 August 1995.[37]

Due to differences in national conventions for rounding and significant digits, all conversion between the national currencies had to be carried out using the process of triangulation via the euro. The definitive values of one euro in terms of the exchange rates at which the currency entered the euro are shown on the right.

The rates were determined by the Council of the European Union,[note 16] based on a recommendation from the European Commission based on the market rates on 31 December 1998. They were set so that one European Currency Unit (ECU) would equal one euro. The European Currency Unit was an accounting unit used by the EU, based on the currencies of the member states; it was not a currency in its own right. They could not be set earlier, because the ECU depended on the closing exchange rate of the non-euro currencies (principally the pound sterling) that day.

The procedure used to fix the conversion rate between the Greek drachma and the euro was different, since the euro by then was already two years old. While the conversion rates for the initial eleven currencies were determined only hours before the euro was introduced, the conversion rate for the Greek drachma was fixed several months beforehand.[note 17]

The currency was introduced in non-physical form (traveller's cheques, electronic transfers, banking, etc.) at midnight on 1 January 1999, when the national currencies of participating countries (the eurozone) ceased to exist independently. Their exchange rates were locked at fixed rates against each other. The euro thus became the successor to the European Currency Unit (ECU). The notes and coins for the old currencies, however, continued to be used as legal tender until new euro notes and coins were introduced on 1 January 2002.

The changeover period during which the former currencies' notes and coins were exchanged for those of the euro lasted about two months, until 28 February 2002. The official date on which the national currencies ceased to be legal tender varied from member state to member state. The earliest date was in Germany, where the mark officially ceased to be legal tender on 31 December 2001, though the exchange period lasted for two months more. Even after the old currencies ceased to be legal tender, they continued to be accepted by national central banks for periods ranging from several years to indefinitely (the latter for Austria, Germany, Ireland, Estonia and Latvia in banknotes and coins, and for Belgium, Luxembourg, Slovenia and Slovakia in banknotes only). The earliest coins to become non-convertible were the Portuguese escudos, which ceased to have monetary value after 31 December 2002, although banknotes remain exchangeable until 2022.

Eurozone crisis[edit]

Budget deficit of the eurozone compared to the United States and the UK.

Following the U.S. financial crisis in 2008, fears of a sovereign debt crisis developed in 2009 among investors concerning some European states, with the situation becoming particularly tense in early 2010.[38][39]Greece was most acutely affected, but fellow Eurozone members Cyprus, Ireland, Italy, Portugal, and Spain were also significantly affected.[40][41] All these countries utilized EU funds except Italy, which is a major donor to the EFSF.[42] To be included in the eurozone, countries had to fulfil certain convergence criteria, but the meaningfulness of such criteria was diminished by the fact it was not enforced with the same level of strictness among countries.[43]

According to the Economist Intelligence Unit in 2011, "[I]f the [euro area] is treated as a single entity, its [economic and fiscal] position looks no worse and in some respects, rather better than that of the US or the UK" and the budget deficit for the euro area as a whole is much lower and the euro area's government debt/GDP ratio of 86% in 2010 was about the same level as that of the United States. "Moreover", they write, "private-sector indebtedness across the euro area as a whole is markedly lower than in the highly leveraged Anglo-Saxon economies". The authors conclude that the crisis "is as much political as economic" and the result of the fact that the euro area lacks the support of "institutional paraphernalia (and mutual bonds of solidarity) of a state".[44]

The crisis continued with S&P downgrading the credit rating of nine euro-area countries, including France, then downgrading the entire European Financial Stability Facility (EFSF) fund.[45]

A historical parallel – to 1931 when Germany was burdened with debt, unemployment and austerity while France and the United States were relatively strong creditors – gained attention in summer 2012[46] even as Germany received a debt-rating warning of its own.[47][48] In the enduring of this scenario the Euro serves as a mean of quantitative primitive accumulation.

Direct and indirect usage[edit]

Direct usage[edit]

The euro is the sole currency of 19 EU member states: Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia, and Spain. These countries constitute the "eurozone", some 343 million people in total as of 2018[update].[49]

With all but two of the remaining EU members obliged to join, together with future members of the EU, the enlargement of the eurozone is set to continue. Outside the EU, the euro is also the sole currency of Montenegro and Kosovo and several European microstates (Andorra, Monaco, San Marino and the Vatican City) as well as in five overseas territories of EU members that are not themselves part of the EU (Saint Barthélemy, Saint Martin, Saint Pierre and Miquelon, the French Southern and Antarctic Lands and Akrotiri and Dhekelia). Together this direct usage of the euro outside the EU affects nearly 3 million people.

The euro has been used as a trading currency in Cuba since 1998,[50] and Syria since 2006.[51] There are also various currencies pegged to the euro (see below). In 2009, Zimbabwe abandoned its local currency and used major currencies instead, including the euro and the United States dollar.[52]

Use as reserve currency[edit]

Since its introduction, the euro has been the second most widely held international reserve currency after the U.S. dollar. The share of the euro as a reserve currency increased from 18% in 1999 to 27% in 2008. Over this period, the share held in U.S. dollar fell from 71% to 64% and that held in Yen fell from 6.4% to 3.3%. The euro inherited and built on the status of the Deutsche Mark as the second most important reserve currency. The euro remains underweight as a reserve currency in advanced economies while overweight in emerging and developing economies: according to the International Monetary Fund[53] the total of euro held as a reserve in the world at the end of 2008 was equal to $1.1 trillion or €850 billion, with a share of 22% of all currency reserves in advanced economies, but a total of 31% of all currency reserves in emerging and developing economies.

The possibility of the euro becoming the first international reserve currency has been debated among economists.[54] Former US Federal Reserve Chairman Alan Greenspan gave his opinion in September 2007 that it was "absolutely conceivable that the euro will replace the US dollar as reserve currency, or will be traded as an equally important reserve currency".[55] In contrast to Greenspan's 2007 assessment, the euro's increase in the share of the worldwide currency reserve basket has slowed considerably since 2007 and since the beginning of the worldwide credit crunch related recession and European sovereign-debt crisis.[53]

Currencies pegged to the euro[edit]

Worldwide use of the euro and the US dollar:

Eurozone

External adopters of the euro

Currencies pegged to the euro

Currencies pegged to the euro within narrow band

United States

External adopters of the US dollar

Currencies pegged to the US dollar

Currencies pegged to the US dollar within narrow band

Note: The Belarusian ruble is pegged to the euro, Russian ruble and US$ in a currency basket.

Outside the eurozone, a total of 22 countries and territories that do not belong to the EU have currencies that are directly pegged to the euro including 14 countries in mainland Africa (CFA franc), two African island countries (Comorian franc and Cape Verdean escudo), three French Pacific territories (CFP franc) and three Balkan countries, Bosnia and Herzegovina (Bosnia and Herzegovina convertible mark), Bulgaria (Bulgarian lev) and Macedonia (Macedonian denar).[56] On 28 July 2009, São Tomé and Príncipe signed an agreement with Portugal which will eventually tie its currency to the euro.[57] Additionally, the Moroccan dirham is tied to a basket of currencies, including the euro and the US dollar, with the euro given the highest weighting.

With the exception of Bosnia, Bulgaria, Macedonia (which had pegged their currencies against the Deutsche Mark) and Cape Verde (formerly pegged to the Portuguese escudo), all of these non-EU countries had a currency peg to the French Franc before pegging their currencies to the euro. Pegging a country's currency to a major currency is regarded as a safety measure, especially for currencies of areas with weak economies, as the euro is seen as a stable currency, prevents runaway inflation and encourages foreign investment due to its stability.

Within the EU several currencies are pegged to the euro, mostly as a precondition to joining the eurozone. The Bulgarian lev was formerly pegged to the Deutsche Mark; one other EU currency with a direct peg due to ERM II is the Danish krone.

In total, as of 2013[update], 182 million people in Africa use a currency pegged to the euro, 27 million people outside the eurozone in Europe, and another 545,000 people on Pacific islands.[49]

Since 2005, stamps issued by the Sovereign Military Order of Malta have been denominated in euros, although the Order's official currency remains the Maltese scudo.[58] The Maltese scudo itself is pegged to the euro and is only recognised as legal tender within the Order.

Economics[edit]

Optimal currency area[edit]

In economics, an optimum currency area, or region (OCA or OCR), is a geographical region in which it would maximise economic efficiency to have the entire region share a single currency. There are two models, both proposed by Robert Mundell: the stationary expectations model and the international risk sharing model. Mundell himself advocates the international risk sharing model and thus concludes in favour of the euro.[59] However, even before the creation of the single currency, there were concerns over diverging economies. Before the late-2000s recession it was considered unlikely that a state would leave the euro or the whole zone would collapse.[60] However the Greek government-debt crisis led to former British Foreign Secretary Jack Straw claiming the eurozone could not last in its current form.[61] Part of the problem seems to be the rules that were created when the euro was set up. John Lanchester, writing for The New Yorker, explains it:

| “ | The guiding principle of the currency, which opened for business in 1999, were supposed to be a set of rules to limit a country's annual deficit to three per cent of gross domestic product, and the total accumulated debt to sixty per cent of G.D.P. It was a nice idea, but by 2004 the two biggest economies in the euro zone, Germany and France, had broken the rules for three years in a row.[62] | ” |

Transaction costs and risks[edit]

| Rank | Currency | ISO 4217 code (symbol) | % daily share (April 2016) |

|---|---|---|---|

1 | USD (US$) | 87.6% | |

2 | EUR (€) | 31.4% | |

3 | JPY (¥) | 21.6% | |

4 | GBP (£) | 12.8% | |

5 | AUD (A$) | 6.9% | |

6 | CAD (C$) | 5.1% | |

7 | CHF (Fr) | 4.8% | |

8 | CNY (元) | 4.0% | |

9 | SEK (kr) | 2.2% | |

10 | NZD (NZ$) | 2.1% | |

11 | MXN ($) | 1.9% | |

12 | SGD (S$) | 1.8% | |

13 | HKD (HK$) | 1.7% | |

14 | NOK (kr) | 1.7% | |

15 | KRW (₩) | 1.7% | |

16 | TRY (₺) | 1.4% | |

17 | RUB (₽) | 1.1% | |

18 | INR (₹) | 1.1% | |

19 | BRL (R$) | 1.0% | |

20 | ZAR (R) | 1.0% | |

| Other | 7.1% | ||

| Total[note 18] | 200.0% | ||

The most obvious benefit of adopting a single currency is to remove the cost of exchanging currency, theoretically allowing businesses and individuals to consummate previously unprofitable trades. For consumers, banks in the eurozone must charge the same for intra-member cross-border transactions as purely domestic transactions for electronic payments (e.g., credit cards, debit cards and cash machine withdrawals).

Financial markets on the continent are expected to be far more liquid and flexible than they were in the past. The reduction in cross-border transaction costs will allow larger banking firms to provide a wider array of banking services that can compete across and beyond the eurozone. However, although transaction costs were reduced, some studies have shown that risk aversion has increased during the last 40 years in the Eurozone.[64]

Price parity[edit]

Another effect of the common European currency is that differences in prices—in particular in price levels—should decrease because of the law of one price. Differences in prices can trigger arbitrage, i.e., speculative trade in a commodity across borders purely to exploit the price differential. Therefore, prices on commonly traded goods are likely to converge, causing inflation in some regions and deflation in others during the transition. Some evidence of this has been observed in specific eurozone markets.[65]

Macroeconomic stability[edit]

Before the introduction of the euro, some countries had successfully contained inflation, which was then seen as a major economic problem, by establishing largely independent central banks. One such bank was the Bundesbank in Germany; the European Central Bank was modelled on the Bundesbank.[66]

The euro has come under criticism due to its imperialistic style regulation, lack of flexibility and [67] rigidity towards sharing member States on issues such as nominal interest rates.

Many national and corporate bonds denominated in euro are significantly more liquid and have lower interest rates than was historically the case when denominated in national currencies. While increased liquidity may lower the nominal interest rate on the bond, denominating the bond in a currency with low levels of inflation arguably plays a much larger role. A credible commitment to low levels of inflation and a stable debt reduces the risk that the value of the debt will be eroded by higher levels of inflation or default in the future, allowing debt to be issued at a lower nominal interest rate.

Unfortunately, there is also a cost in structurally keeping inflation lower than in the United States, UK, and China. The result is that seen from those countries, the euro has become expensive, making European products increasingly expensive for its largest importers. Hence export from the euro zone becomes more difficult.

In general, those in Europe who own large amounts of euros are served by high stability and low inflation.

A monetary union means countries lose the main mechanism of recovery of their international competitiveness by weakening (depreciating) their currency. When wages become too high compared to productivity in exports sector then these exports become more expensive and they are crowded out from the market within a country and abroad. This drive fall of employment and output in exports sector and fall of trade and current account balances. Fall of output and employment in tradable goods sector may be offset by growth of non-exports sectors, especially in construction and services. Increased purchases abroad and negative current account balance can be financed without a problem as long as credit is cheap. [68] The need to finance trade deficit weakens currency making exports automatically more attractive in a country and abroad. A country in a monetary union cannot use weakening of currency to recover its international competitiveness. To achieve this a country has to reduce prices, including wages (deflation). This means years of high unemployment and lower incomes as it was during European sovereign-debt crisis. [69]

Trade[edit]

A 2009 consensus from the studies of the introduction of the euro concluded that it has increased trade within the eurozone by 5% to 10%,[70] although one study suggested an increase of only 3%[71] while another estimated 9 to 14%.[72] However, a meta-analysis of all available studies suggests that the prevalence of positive estimates is caused by publication bias and that the underlying effect may be negligible.[73] Furthermore, studies accounting for time trend reflecting general cohesion policies in Europe that started before, and continue after implementing the common currency find no effect on trade.[74][75] These results suggest that other policies aimed at European integration might be the source of observed increase in trade.

Investment[edit]

Physical investment seems to have increased by 5% in the eurozone due to the introduction.[76] Regarding foreign direct investment, a study found that the intra-eurozone FDI stocks have increased by about 20% during the first four years of the EMU.[77] Concerning the effect on corporate investment, there is evidence that the introduction of the euro has resulted in an increase in investment rates and that it has made it easier for firms to access financing in Europe. The euro has most specifically stimulated investment in companies that come from countries that previously had weak currencies. A study found that the introduction of the euro accounts for 22% of the investment rate after 1998 in countries that previously had a weak currency.[78]

Inflation[edit]

The introduction of the euro has led to extensive discussion about its possible effect on inflation. In the short term, there was a widespread impression in the population of the eurozone that the introduction of the euro had led to an increase in prices, but this impression was not confirmed by general indices of inflation and other studies.[79][80] A study of this paradox found that this was due to an asymmetric effect of the introduction of the euro on prices: while it had no effect on most goods, it had an effect on cheap goods which have seen their price round up after the introduction of the euro. The study found that consumers based their beliefs on inflation of those cheap goods which are frequently purchased.[81] It has also been suggested that the jump in small prices may be because prior to the introduction, retailers made fewer upward adjustments and waited for the introduction of the euro to do so.[82]

Exchange rate risk[edit]

One of the advantages of the adoption of a common currency is the reduction of the risk associated with changes in currency exchange rates. It has been found that the introduction of the euro created "significant reductions in market risk exposures for nonfinancial firms both in and outside Europe".[83] These reductions in market risk "were concentrated in firms domiciled in the eurozone and in non-euro firms with a high fraction of foreign sales or assets in Europe".

Financial integration[edit]

The introduction of the euro seems to have had a strong effect on European financial integration. According to a study on this question, it has "significantly reshaped the European financial system, especially with respect to the securities markets [...] However, the real and policy barriers to integration in the retail and corporate banking sectors remain significant, even if the wholesale end of banking has been largely integrated."[84] Specifically, the euro has significantly decreased the cost of trade in bonds, equity, and banking assets within the eurozone.[85] On a global level, there is evidence that the introduction of the euro has led to an integration in terms of investment in bond portfolios, with eurozone countries lending and borrowing more between each other than with other countries.[86]

Effect on interest rates[edit]

Secondary market yields of government bonds with maturities of close to 10 years

As of January 2014, and since the introduction of the euro, interest rates of most member countries (particularly those with a weak currency) have decreased. Some of these countries had the most serious sovereign financing problems.

The effect of declining interest rates, combined with excess liquidity continually provided by the ECB, made it easier for banks within the countries in which interest rates fell the most, and their linked sovereigns, to borrow significant amounts (above the 3% of GDP budget deficit imposed on the eurozone initially) and significantly inflate their public and private debt levels.[87] Following the financial crisis of 2007–2008, governments in these countries found it necessary to bail out or nationalise their privately held banks to prevent systemic failure of the banking system when underlying hard or financial asset values were found to be grossly inflated and sometimes so near worthless there was no liquid market for them.[88] This further increased the already high levels of public debt to a level the markets began to consider unsustainable, via increasing government bond interest rates, producing the ongoing European sovereign-debt crisis.

Price convergence[edit]

The evidence on the convergence of prices in the eurozone with the introduction of the euro is mixed. Several studies failed to find any evidence of convergence following the introduction of the euro after a phase of convergence in the early 1990s.[89][90] Other studies have found evidence of price convergence,[91][92] in particular for cars.[93] A possible reason for the divergence between the different studies is that the processes of convergence may not have been linear, slowing down substantially between 2000 and 2003, and resurfacing after 2003 as suggested by a recent study (2009).[94]

Tourism[edit]

A study suggests that the introduction of the euro has had a positive effect on the amount of tourist travel within the EMU, with an increase of 6.5%.[95]

Exchange rates[edit]

Flexible exchange rates[edit]

The ECB targets interest rates rather than exchange rates and in general does not intervene on the foreign exchange rate markets. This is because of the implications of the Mundell–Fleming model, which implies a central bank cannot (without capital controls) maintain interest rate and exchange rate targets simultaneously, because increasing the money supply results in a depreciation of the currency. In the years following the Single European Act, the EU has liberalised its capital markets and, as the ECB has inflation targeting as its monetary policy, the exchange-rate regime of the euro is floating.

Against other major currencies[edit]

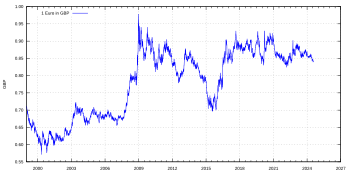

The euro is the second-most widely held reserve currency after the U.S. dollar. After its introduction on 4 January 1999 its exchange rate against the other major currencies fell reaching its lowest exchange rates in 2000 (3 May vs Pound sterling, 25 October vs the U.S. dollar, 26 October vs Japanese yen). Afterwards it regained and its exchange rate reached its historical highest point in 2008 (15 July vs U.S. dollar, 23 July vs Japanese yen, 29 December vs Pound sterling). With the advent of the global financial crisis the euro initially fell, to regain later. Despite pressure due to the European sovereign-debt crisis the euro remained stable.[96] In November 2011 the euro's exchange rate index – measured against currencies of the bloc's major trading partners – was trading almost two percent higher on the year, approximately at the same level as it was before the crisis kicked off in 2007.[97]

@media all and (max-width:720px).mw-parser-output .tmulti>.thumbinnerwidth:100%!important;max-width:none!important.mw-parser-output .tmulti .tsinglefloat:none!important;max-width:none!important;width:100%!important;text-align:center

- Current and historical exchange rates against 32 other currencies (European Central Bank): link

| Current EUR exchange rates | |

|---|---|

| From Google Finance: | AUD CAD CHF GBP HKD JPY USD RUB INR CNY |

| From Yahoo! Finance: | AUD CAD CHF GBP HKD JPY USD RUB INR CNY |

| From XE: | AUD CAD CHF GBP HKD JPY USD RUB INR CNY |

| From OANDA: | AUD CAD CHF GBP HKD JPY USD RUB INR CNY |

| From fxtop.com: | AUD CAD CHF GBP HKD JPY USD RUB INR CNY |

Linguistic issues[edit]

5 euro note from the new Europa series written in Latin (EURO) and Greek (ΕΥΡΩ) alphabets, but also in the Cyrillic (ЕВРО) alphabet, as a result of Bulgaria joining the European Union in 2007.

The formal titles of the currency are euro for the major unit and cent for the minor (one-hundredth) unit and for official use in most eurozone languages; according to the ECB, all languages should use the same spelling for the nominative singular.[98] This may contradict normal rules for word formation in some languages, e.g., those in which there is no eu diphthong. Bulgaria has negotiated an exception; euro in the Bulgarian Cyrillic alphabet is spelled as eвро (evro) and not eуро (euro) in all official documents.[99] In the Greek script the term ευρώ (evró) is used; the Greek "cent" coins are denominated in λεπτό/ά (leptó/á). Official practice for English-language EU legislation is to use the words euro and cent as both singular and plural,[100] although the European Commission's Directorate-General for Translation states that the plural forms euros and cents should be used in English.[101]

See also[edit]

- Currency union

- List of currencies replaced by the euro

- List of currencies in Europe

- Captain Euro

Notes[edit]

^ €100 and €200 notes from the Europa series will start circulating on 28 May 2019, €500 note is discontinued

^ Except Northern Cyprus that uses Turkish lira

^ Including overseas departments (French Guiana, Guadeloupe, Martinique, Mayotte and Réunion)

^ Except the Italian exclave of Campione d'Italia in Switzerland that uses the Swiss franc.

^ Only the European part of the country is part of the European Union and uses the euro. The Caribbean Netherlands introduced the United States dollar in 2011. Curaçao, Sint Maarten and Aruba have their own currencies, which are pegged to the dollar.

^ "Monetary Agreement between the European Union and the Principality of Andorra". Official Journal of the European Union. 17 December 2011. Retrieved 2012-09-08..mw-parser-output cite.citationfont-style:inherit.mw-parser-output .citation qquotes:"""""""'""'".mw-parser-output .citation .cs1-lock-free abackground:url("//upload.wikimedia.org/wikipedia/commons/thumb/6/65/Lock-green.svg/9px-Lock-green.svg.png")no-repeat;background-position:right .1em center.mw-parser-output .citation .cs1-lock-limited a,.mw-parser-output .citation .cs1-lock-registration abackground:url("//upload.wikimedia.org/wikipedia/commons/thumb/d/d6/Lock-gray-alt-2.svg/9px-Lock-gray-alt-2.svg.png")no-repeat;background-position:right .1em center.mw-parser-output .citation .cs1-lock-subscription abackground:url("//upload.wikimedia.org/wikipedia/commons/thumb/a/aa/Lock-red-alt-2.svg/9px-Lock-red-alt-2.svg.png")no-repeat;background-position:right .1em center.mw-parser-output .cs1-subscription,.mw-parser-output .cs1-registrationcolor:#555.mw-parser-output .cs1-subscription span,.mw-parser-output .cs1-registration spanborder-bottom:1px dotted;cursor:help.mw-parser-output .cs1-ws-icon abackground:url("//upload.wikimedia.org/wikipedia/commons/thumb/4/4c/Wikisource-logo.svg/12px-Wikisource-logo.svg.png")no-repeat;background-position:right .1em center.mw-parser-output code.cs1-codecolor:inherit;background:inherit;border:inherit;padding:inherit.mw-parser-output .cs1-hidden-errordisplay:none;font-size:100%.mw-parser-output .cs1-visible-errorfont-size:100%.mw-parser-output .cs1-maintdisplay:none;color:#33aa33;margin-left:0.3em.mw-parser-output .cs1-subscription,.mw-parser-output .cs1-registration,.mw-parser-output .cs1-formatfont-size:95%.mw-parser-output .cs1-kern-left,.mw-parser-output .cs1-kern-wl-leftpadding-left:0.2em.mw-parser-output .cs1-kern-right,.mw-parser-output .cs1-kern-wl-rightpadding-right:0.2em

^ "By monetary agreement between France (acting for the EC) and Monaco". Retrieved 30 May 2010.

^ "By monetary agreement between Italy (acting for the EC) and San Marino". Retrieved 30 May 2010.

^ "By monetary agreement between Italy (acting for the EC) and Vatican City". Retrieved 30 May 2010.

^ "By the third protocol to the Cyprus adhesion Treaty to EU and British local ordinance" (PDF). Retrieved 17 July 2011.

^ "By agreement of the EU Council". Retrieved 30 May 2010.

^ "By UNMIK administration direction 1999/2". Unmikonline.org. Archived from the original on 7 June 2011. Retrieved 30 May 2010.

^ See Montenegro and the euro

^ As of 26 April 2013[update]:

Total EUR currency (coins and banknotes) in circulation 771.5 (banknotes) + 21.032 (coins) =792.53 billion EUR * 1.48 (exchange rate) = 1,080 billion USD

Total USD currency (coins and banknotes) in circulation 859 billion USD

"Table 2: Euro banknotes, values (EUR billions, unless otherwise indicated, not seasonally adjusted)" (PDF). European Central Bank. Archived from the original (PDF) on 22 February 2010. Retrieved 13 December 2009.2009, October: Total banknotes: 771.5 (billion EUR)

"Table 4: Euro coins, values (EUR millions, unless otherwise indicated, not seasonally adjusted)" (PDF). European Central Bank. Archived from the original (PDF) on 22 February 2010. Retrieved 13 December 2009.2009, October: Total coins: 21,032 (million EUR)

"Money Stock Measures". Federal Reserve Statistical Release. Board of Governors of the Federal Reserve System. Retrieved 13 December 2009.Table 5: Not Seasonally Adjusted Components of M1 (Billions of dollars), not seasonally adjusted, October 2009: Currency: 859.3 (billion USD)

"Euro foreign exchange reference rates". European Central Bank. Retrieved 13 December 2009.Exchange rate 2009-10-30: 1 EUR = 1.48 USD

^ In the quotation, the epsilon is actually represented with the Cyrillic capital letter Ukrainian ye (Є, U+0404) instead of the technically more appropriate Greek lunate epsilon symbol (ϵ, U+03F5).

^ by means of Council Regulation 2866/98 (EC) of 31 December 1998.

^ by Council Regulation 1478/2000 (EC) of 19 June 2000

^ The total sum is 200% because each currency trade always involves a currency pair.

References[edit]

^ Official documents and legislation refer to the euro as "the single currency".

"Council Regulation (EC) No 1103/97 of 17 June 1997 on certain provisions relating to the introduction of the euro". Official Journal L 162, 19 June 1997 P. 0001 – 0003. European Communities. 19 June 1997. Retrieved 1 April 2009.

This term is sometimes adopted by the media (Google hits for the phrase)

^ "Currency nicknames".

^ "In Zimbabwe there are nine currencies, amongst others the euro and the US dollar". uselessk.com. Archived from the original on 15 January 2015. Retrieved 29 May 2014.

^ "Currently, the South African rand, Botswana pula, pound sterling, euro, and the United States dollar are all in use". geocurrents.info. Retrieved 29 May 2014.

^ The Belarusian ruble is pegged to the euro, Russian ruble and US$ in a currency basket.

^ Cardoso, Paulo. "Interview – Governor of the National Bank of Macedonia – Dimitar Bogov". The American Times United States Emerging Economies Report (USEER Report). Hazlehurst Media SA. Retrieved 8 September 2013.

^ "The euro". European Commission website. Retrieved 2 January 2019.

^ ab "What is the euro area?". European Commission website. Retrieved 2019-01-02.

^ "Foreign exchange turnover in April 2013: preliminary global results" (PDF). Bank for International Settlements. Retrieved 7 February 2015.

^ "Triennial Central Bank Survey 2007" (PDF). BIS. 19 December 2007. Retrieved 25 July 2009.

^ Aristovnik, Aleksander; Čeč, Tanja (30 March 2010). "Compositional Analysis of Foreign Currency Reserves in the 1999–2007 Period. The Euro vs. The Dollar As Leading Reserve Currency" (PDF). Munich Personal RePEc Archive, Paper No. 14350. Retrieved 27 December 2010.

^ Boesler, Matthew (11 November 2013). "There Are Only Two Real Threats To The US Dollar's Status As The International Reserve Currency". Business Insider. Retrieved 8 December 2013.

^ "Banknotes and coins circulation". European Central Bank. Retrieved 28 August 2018.

^ ab "Madrid European Council (12/95): Conclusions". European Parliament. Retrieved 14 February 2009.

^ "Initial changeover (2002)". European Central Bank. Retrieved 5 March 2011.

^ "Exchange Rate Average (US Dollar, Euro) – X-Rates". X-rates.com. Retrieved 2013-03-12.

^ "The Euro". European Commission. Retrieved 29 January 2009.

^ abc Scheller, Hanspeter K. (2006). The European Central Bank: History, Role and Functions (pdf) (2nd ed.). p. 103. ISBN 92-899-0027-X.Since 1 January 2002, the NCBs and the ECB have issued euro banknotes on a joint basis.

^

"Capital Subscription". European Central Bank. Retrieved 18 December 2011.The NCBs' shares in this capital are calculated using a key which reflects the respective country's share in the total population and gross domestic product of the EU – in equal weightings. The ECB adjusts the shares every five years and whenever a new country joins the EU. The adjustment is done on the basis of data provided by the European Commission.

^ ab "How to use the euro name and symbol". European Commission. Retrieved 7 April 2010.

^ European Commission. "Spelling of the words "euro" and "cent" in official Community languages as used in Community Legislative acts" (PDF). Retrieved 26 November 2008.

^ European Commission Directorate-General for Translation. "English Style Guide: A handbook for authors and translators in the European Commission" (PDF). Archived from the original (PDF) on 5 December 2010. Retrieved 16 November 2008.; European Union. "Interinstitutional style guide, 7.3.3. Rules for expressing monetary units". Retrieved 16 November 2008.

^ "Ireland to round to nearest 5 cents starting October 28". 27 October 2015. Archived from the original on 6 March 2016. Retrieved 17 December 2018.

^ "Rounding". Central Bank of Ireland.

^ European Commission (January 2007). "Euro cash: five and familiar". Europa. Retrieved 26 January 2009.

^ Pop, Valentina (22 March 2010) "Commission frowns on shop signs that say: '€500 notes not accepted'", EU Observer

^ European Commission (15 February 2003). "Commission communication: The introduction of euro banknotes and coins one year after COM(2002) 747". Europa (web portal). Retrieved 26 January 2009.

^ "Robert Kalina, designer of the euro banknotes, at work at the Oesterreichische Nationalbank in Vienna". European Central Bank. Retrieved 30 May 2010.

^ Schmid, John (3 August 2001). "Etching the Notes of a New European Identity". International Herald Tribune. Retrieved 29 May 2009.

^ "Regulation (EC) No 2560/2001 of the European Parliament and of the Council of 19 December 2001 on cross-border payments in euro". EUR-lex – European Communities, Publications office, Official Journal L 344, 28 December 2001 P. 0013 – 0016. Retrieved 26 December 2008.

^ "Cross border payments in the EU, Euro Information, The Official Treasury Euro Resource". United Kingdom Treasury. Archived from the original on 1 December 2008. Retrieved 26 December 2008.

^ European Central Bank. "TARGET". Archived from the original on 21 January 2008. Retrieved 25 October 2007.

^ "The €uro: Our Currency". European Commission. Archived from the original on 11 October 2007. Retrieved 25 October 2007.

^ Siebert, Jürgen (2002). "The Euro: From Logo to Letter". Font Magazine (2).

^ "Position of the ISO code or euro sign in amounts". Interinstitutional style guide. Bruxelles, Belgium: Europa Publications Office. 5 February 2009. Retrieved 10 January 2010.

^ "Fixed Euro conversion rates". European Central Bank. Retrieved 6 August 2011.

^ "Germain Pirlot 'uitvinder' van de euro" (in Dutch). De Zeewacht. 16 February 2007. Archived from the original on 30 June 2013. Retrieved 21 May 2012.

^ George Matlock (16 February 2010). "Peripheral euro zone government bond spreads widen". Reuters. Retrieved 28 April 2010.

^ "Acropolis now". The Economist. 29 April 2010. Retrieved 22 June 2011.

^ European Debt Crisis Fast Facts, CNN Library (last updated 22 January 2017).

^ Ricardo Reis, Looking for a Success in the Euro Crisis Adjustment Programs: The Case of Portugal, Brookings Papers on Economic Activity, Brookings Institution (Fall 2015), p. 433.

^ "Efsf, come funziona il fondo salvastati europeo". 4 November 2011.

^ "The politics of the Maastricht convergence criteria". Voxeu.org. 15 April 2009. Retrieved 1 October 2011.

^ "State of the Union: Can the euro zone survive its debt crisis?" (PDF). Economist Intelligence Unit. 1 March 2011. p. 4. Retrieved 1 December 2011.

^ "S&P downgrades euro zone's EFSF bailout fund". Reuters. 2017-01-16. Retrieved 2017-01-21.

^ Delamaide, Darrell (24 July 2012). "Euro crisis brings world to brink of depression". MarketWatch. Retrieved 24 July 2012.

^ Lindner, Fabian, "Germany would do well to heed the Moody's warning shot", The Guardian, 24 July 2012. Retrieved 25 July 2012.

^ Buergin, Rainer, "Germany, Juncker Push Back After Moody’s Rating Outlook Cuts Archived 28 July 2012 at the Wayback Machine", washpost.bloomberg, 24 July 2012. Retrieved 25 July 2012.

^ ab Population Reference Bureau. "2013 World Population Data Sheet" (PDF). Retrieved 2013-10-01.

^ "Cuba to adopt euro in foreign trade". BBC News. 8 November 1998. Retrieved 2 January 2008.

^ "US row leads Syria to snub dollar". BBC News. 14 February 2006. Retrieved 2 January 2008.

^ "Zimbabwe: A Critical Review of Sterp". 17 April 2009. Retrieved 30 April 2009.

^ ab "Currency Composition of Official Foreign Exchange Reserves (COFER) – Updated COFER tables include first quarter 2009 data. June 30, 2009" (PDF). Retrieved 8 July 2009.

^ "Will the Euro Eventually Surpass the Dollar As Leading International Reserve Currency?" (PDF). Archived from the original (PDF) on 25 August 2013. Retrieved 17 July 2011.

^ "Euro could replace dollar as top currency – Greenspan". Reuters. 17 September 2007. Retrieved 17 September 2007.

^ Cardoso, Paulo. "Interview – Governor of the National Bank of Macedonia – Dimitar Bogov". The American Times United States Emerging Economies Report (USEER Report). Hazlehurst Media SA. Retrieved 8 September 2013.

^ "S.Tomé e Princípe ancora-se ao euro". economia.publico.pt. 27 July 2009. Retrieved 8 November 2011.

^ https://www.orderofmalta.int/associate-countries/ Retrieved 3 October 2017.

^ A Plan for a European Currency, 1973 by Mundell

^ "The Breakup of the Euro Area by Barry Eichengreen". 14 September 2007. SSRN 1014341. NBER Working Paper No. w13393.

^ "Greek debt crisis: Straw says eurozone 'will collapse'". BBC. 20 June 2011. Retrieved 17 July 2011.

^ John Lanchester, "Euro Science," New Yorker, 10 October 2011.

^ "Triennial Central Bank Survey Foreign exchange turnover in April 2016" (PDF). Triennial Central Bank Survey. Basel, Switzerland: Bank for International Settlements. 11 December 2016. p. 7. Retrieved 22 March 2017.

^ Benchimol, J., 2014. Risk aversion in the Eurozone, Research in Economics, vol. 68, issue 1, pp. 39–56.

^ Goldberg, Pinelopi K.; Verboven, Frank (2005). "Market Integration and Convergence to the Law of One Price: Evidence from the European Car Market". Journal of International Economics. 65 (1): 49–73. doi:10.1016/j.jinteco.2003.12.002.

^ de Haan, Jakob (2000). The History of the Bundesbank: Lessons for the European Central Bank. London: Routledge. ISBN 978-0-415-21723-1.

^ Silvia, Steven J (2004). "Is the Euro Working? The Euro and European Labour Markets". Journal of Public Policy. 24 (2): 147–168. doi:10.1017/s0143814x0400008x. JSTOR 4007858.

^ Ernest Pytlarczyk, Stefan Kawalec (June 2012). "Controlled Dismantlement of the Euro Area in Order to Preserve the European Union and Single European Market". CASE Center for Social and Economic Research. p. 11. Retrieved 19 December 2018.

^ Martin Feldstein (January–February 2012). "The Failure of the Euro". Foreign Affairs. Chapter: Trading Places.CS1 maint: Date format (link)

^ "The euro's trade effects" (PDF). Retrieved 2 October 2009.

^ "The Euro Effect on Trade is not as Large as Commonly Thought" (PDF). Archived from the original (PDF) on 24 July 2011. Retrieved 2 October 2009.

^ Chintrakarn, Pandej (2007). "Estimating the Euro Effects on Trade with Propensity Score Matching". Review of International Economics. 16: 186–198. doi:10.1111/j.1467-9396.2007.00725.x. SSRN 1079383.

^ Havránek, Tomáš (2010). "Rose effect and the euro: is the magic gone?". Review of World Economics. 146 (2): 241–261. doi:10.1007/s10290-010-0050-1. Retrieved 13 July 2010.

^ Gomes, Tamara; Graham, Chris; Helliwel, John; Takashi, Kano; Murray, John; Schembri, Lawrence (August 2006). "The Euro and Trade: Is there a Positive Effect?" (PDF). Bank of Canada. Archived from the original (PDF) on 3 September 2015.

^ H., Berger; V., Nitsch (2008). "Zooming out: The trade effect of the euro in historical perspective". Journal of International Money and Finance. 27 (8): 1244–1260. doi:10.1016/j.jimonfin.2008.07.005.

^ "The Impact of the Euro on Investment: Sectoral Evidence" (PDF). Archived from the original (PDF) on 31 August 2013. Retrieved 2 October 2009.

^ "Does the single currency affect FDI?" (PDF). AFSE.fr. Archived from the original (PDF) on 22 February 2010. Retrieved 30 May 2010.

^ "The Real Effects of the Euro: Evidence from Corporate Investments" (PDF). Archived from the original (PDF) on 6 July 2011. Retrieved 30 May 2010.

^ Paolo Angelini; Francesco Lippi (December 2007). "Did Prices Really Soar after the Euro Cash Changeover? Evidence from ATM Withdrawals" (PDF). International Journal of Central Banking. Retrieved 23 August 2011.

^ Irmtraud Beuerlein. "Fünf Jahre nach der Euro-Bargeldeinführung –War der Euro wirklich ein Teuro?" [Five years after the introduction of euro cash – Did the euro really make things more expensive?] (PDF) (in German). Statistisches Bundesamt, Wiesbaden. Retrieved 23 August 2011.

^ Dziuda, Wioletta; Mastrobuoni, Giovanni (2009). "The Euro Changeover and Its Effects on Price Transparency and Inflation". Journal of Money, Credit and Banking. 41: 101–129. doi:10.1111/j.1538-4616.2008.00189.x. Retrieved 12 November 2010.

^ Hobijn, Bart; Ravenna, Federico; Tambalotti, Andrea (2006). "Quarterly Journal of Economics – Abstract". Quarterly Journal of Economics. MIT Press Journals. 121 (3): 1103–1131. doi:10.1162/qjec.121.3.1103.

^ Bartram, Söhnke M.; Karolyi, G. Andrew (2006). "The impact of the introduction of the Euro on foreign exchange rate risk exposures". Journal of Empirical Finance. 13 (4–5): 519–549. doi:10.1016/j.jempfin.2006.01.002.

^ "The Euro and Financial Integration" (PDF). May 2006. Retrieved 2 October 2009.

^ Coeurdacier, Nicolas; Martin, Philippe (2009). "The geography of asset trade and the euro: Insiders and outsiders". Journal of the Japanese and International Economies. 23 (2): 90–113. doi:10.1016/j.jjie.2008.11.001.

^ Philip R. Lane (22 August 2006). "Global Bond Portfolios and EMU". SSRN 925858. IIIS Discussion Paper No. 168.

^ "Redwood: The origins of the euro crisis". Investmentweek.co.uk. 3 June 2011. Retrieved 16 September 2011.

^ "Farewell, Fair-Weather Euro | IP – Global-Edition". Ip-global.org. Archived from the original on 17 March 2011. Retrieved 16 September 2011.

^ "Price setting and inflation dynamics: did EMU matter" (PDF). Retrieved 13 March 2011.

^ "Price convergence in the EMU? Evidence from micro data" (PDF). Retrieved 2 October 2009.

^ "One TV, One Price?" (PDF). Retrieved 17 July 2011.

^ "One Market, One Money, One Price?" (PDF). Retrieved 17 July 2011.

^ Gil-Pareja, Salvador, and Simón Sosvilla-Rivero, "Price Convergence in the European Car Market", FEDEA, November 2005.

^ Fritsche, Ulrich; Lein, Sarah; Weber, Sebastian (April 2009). "Do Prices in the EMU Converge (Non-linearly)?" (PDF). University of Hamburg, Department Economics and Politics Discussion Papers, Macroeconomics and Finance Series. Archived from the original (PDF) on 19 July 2011. Retrieved 28 December 2010.

^ Gil-Pareja, Salvador; Llorca-Vivero, Rafael; Martínez-Serrano, José (May 2007). "The Effect of EMU on Tourism". Review of International Economics. 15 (2): 302–312. SSRN 983231.

^ Kirschbaum, Erik. "Schaeuble says markets have confidence in euro". Reuters. Retrieved 28 March 2018.

^ "Puzzle over euro's 'mysterious' stability". Reuters. 15 November 2011.

^ "European Central Bank, Convergence Report" (PDF). May 2007. Retrieved 29 December 2008.The euro is the single currency of the member states that have adopted it. To make this singleness apparent, Community law requires a single spelling of the word euro in the nominative singular case in all community and national legislative provisions, taking into account the existence of different alphabets.

^ Elena Koinova (19 October 2007). ""Evro" Dispute Over – Portuguese Foreign Minister – Bulgaria". The Sofia Echo. Retrieved 17 July 2011.

^ European Commission. "Spelling of the words "euro" and "cent" in official community languages as used in community legislative acts" (PDF). Retrieved 12 January 2009.

^ For example, see European Commission, Directorate General for Translation: English Style Guide section 22.9 "The euro. Like 'pound', 'dollar' or any other currency name in English, the word 'euro' is written in lower case with no initial capital and, where appropriate, takes the plural 's' (as does 'cent')." European Commission Directorate-General for Translation – English Style Guide Archived 5 December 2010 at the Wayback Machine.

Further reading[edit]

Bartram, Söhnke M.; Taylor, Stephen J.; Wang, Yaw-Huei (May 2007). "The Euro and European Financial Market Dependence". Journal of Banking and Finance. 51 (5): 1461–1481. SSRN 924333.

Bartram, Söhnke M.; Karolyi, G. Andrew (October 2006). "The Impact of the Introduction of the Euro on Foreign Exchange Rate Risk Exposures". Journal of Empirical Finance. 13 (4–5): 519–549. doi:10.1016/j.jempfin.2006.01.002. SSRN 299641.

Baldwin, Richard; Wyplosz, Charles (2004). The Economics of European Integration. New York: McGraw Hill. ISBN 0-07-710394-7.

Buti, Marco; Deroose, Servaas; Gaspar, Vitor; Nogueira Martins, João (2010). The Euro. Cambridge: Cambridge University Press. ISBN 978-92-79-09842-0.

Jordan, Helmuth (2010). "Fehlschlag Euro". Dorrance Publishing. Archived from the original on 16 September 2010. Retrieved 28 January 2011.

Simonazzi, A.; Vianello, F. (2001). "Financial Liberalization, the European Single Currency and the Problem of Unemployment". In Franzini, R.; Pizzuti, R.F. Globalization, Institutions and Social Cohesion. Springer. ISBN 3-540-67741-0.

External links[edit]

Euroat Wikipedia's sister projects

Definitions from Wiktionary

Definitions from Wiktionary

Media from Wikimedia Commons

Media from Wikimedia Commons

News from Wikinews

News from Wikinews

Quotations from Wikiquote

Quotations from Wikiquote

Texts from Wikisource

Texts from Wikisource

Textbooks from Wikibooks

Textbooks from Wikibooks

Resources from Wikiversity

Resources from Wikiversity

- Eurozone official portal

The euro – Europa- European Central Bank – Euro Exchange Rates

- European Central Bank

Euro topics | |||||

|---|---|---|---|---|---|

| General |

| ||||

| Administration |

| ||||

| Fiscal provisions |

| ||||

| History |

| ||||

| Economy |

| ||||

| International status |

| ||||

| Denominations |

| ||||

| Coins by issuing country |

| ||||

Potential adoption by other countries |

| ||||

| Currencies yielded |

| ||||

Currencies remaining |

| ||||

| |||||

Authority control |

|

|---|

Categories:

- ISO 4217

- Currencies of Europe

- Circulating currencies

- Currencies of Africa

- Currencies of Asia

- Euro

- 1999 in economics

- Currency introduced in 1999

- Currency introduced in 2002

- Currencies of the Commonwealth of Nations

- Currencies of South America

- Currencies of the Caribbean

- Currencies of Zimbabwe

- Currency unions

- Economy of the European Union

- Eurozone

- Symbols of the European Union

(window.RLQ=window.RLQ||).push(function()mw.config.set("wgPageParseReport":"limitreport":"cputime":"2.588","walltime":"3.167","ppvisitednodes":"value":35046,"limit":1000000,"ppgeneratednodes":"value":0,"limit":1500000,"postexpandincludesize":"value":908113,"limit":2097152,"templateargumentsize":"value":201681,"limit":2097152,"expansiondepth":"value":21,"limit":40,"expensivefunctioncount":"value":46,"limit":500,"unstrip-depth":"value":1,"limit":20,"unstrip-size":"value":322118,"limit":5000000,"entityaccesscount":"value":4,"limit":400,"timingprofile":["100.00% 2334.256 1 -total"," 30.21% 705.270 2 Template:Reflist"," 16.90% 394.543 1 Template:Infobox_currency"," 16.12% 376.294 1 Template:Infobox"," 14.26% 332.754 1 Template:Politics_of_the_European_Union"," 13.94% 325.363 169 Template:Flagicon"," 13.89% 324.291 1 Template:Sidebar_with_collapsible_lists"," 12.53% 292.503 68 Template:Cite_web"," 11.85% 276.628 11 Template:Collapsible_list"," 8.48% 198.057 16 Template:Cite_journal"],"scribunto":"limitreport-timeusage":"value":"0.855","limit":"10.000","limitreport-memusage":"value":11129504,"limit":52428800,"limitreport-logs":"table#1 nn","cachereport":"origin":"mw1321","timestamp":"20190204024302","ttl":2073600,"transientcontent":false););"@context":"https://schema.org","@type":"Article","name":"Euro","url":"https://en.wikipedia.org/wiki/Euro","sameAs":"http://www.wikidata.org/entity/Q4916","mainEntity":"http://www.wikidata.org/entity/Q4916","author":"@type":"Organization","name":"Contributors to Wikimedia projects","publisher":"@type":"Organization","name":"Wikimedia Foundation, Inc.","logo":"@type":"ImageObject","url":"https://www.wikimedia.org/static/images/wmf-hor-googpub.png","datePublished":"2001-10-09T15:16:08Z","dateModified":"2019-01-31T14:02:57Z","image":"https://upload.wikimedia.org/wikipedia/commons/3/30/Euro_Series_Banknotes.png","headline":"European currency"(window.RLQ=window.RLQ||).push(function()mw.config.set("wgBackendResponseTime":168,"wgHostname":"mw1330"););